Odisha State Board CHSE Odisha Class 12 Economics Solutions Chapter 1 Definition of Economics and Central Problems of An Economy Questions and Answers.

CHSE Odisha 12th Class Economics Chapter 1 Question Answer Definition of Economics and Central Problems of An Economy

Group – A

Short type Questions with Answers

I. Answer within Two/Three sentence.

Question 1.

What is the meaning of the term ‘Economics’ ?

Answer:

The term “Economics” is originally derived from Greek words “Oikis” which means ! iousehold” & “Nemein” which means “Management”. As such, economics is referred as management, of household.

Question 2.

Write down the wealth definition given by Adam Smith.

Answer:

The first systematic definition of economics is given by Adam Smith , the father of economics in his masterpiece “An Enquiry into the Nature and Causes of wealth of Nations” published in 1776. He defined economics as “Science of Wealth” . It includes the acquisition, accumulation and spending of wealth.

Question 3.

Describe Welfare definition of Alfred Marshall.

Answer:

Alfred Marshall propounded a new definition with different touch in his book “ Principles of Economics” published in 1890. His definition is accepted as “Welfare Definition.”

According to Dr. Marshall “ Economics is a study of mankind in ordinary business of life; it examines that part of individual & social actiuon which is most closely connected with the attainment and with the use of material requisites of well being.”

Question 4.

What is Scarcity definition ?

Answer:

The scarcity definition has been enunciated by Lionel Robbins in his book “Essay on the Nature and Significance of Economic Science” published in the year 1932.

According to Robbins, “Economics is a science which studies the human behaviour as a relationship between ends and scarce means which have alternative uses.”

Question 5.

What is the classical view on Subject matter of economics ?

Answer:

Subject matter of economics is a controversial subject. That is why Mrs. Barbara Wooton said, “Whenever six economists are gathered, there are seven opinions.” The classical economists like Adam Smith, J.S. Mill, David Ricardo, LB. Say regarded economics as a science which studied wealth. They considered only material goods as wealth. And wealth formed the subject matter of economics.

Question 6.

What is the Central Problems of Economics ?

Answer:

the origin of the economic problem is in scarcity of resources Multiplicity of end forces on us the problem of choice among the ends so that the most intense among them are satisfied now.

![]()

Question 7.

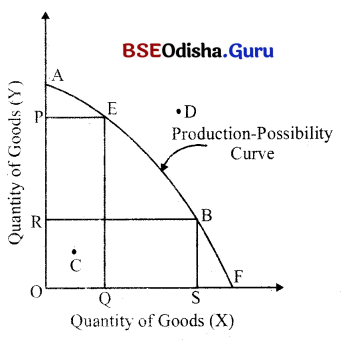

What is Production Possibility Curve ?

Answer:

A production-possibilities curve shows the various combinations of the goods which an economy can produce with given resources and under the given technology. It is a downwards sloping curve which is concave to the origin.

II. Answer within Five/Six sentence :

Question 1.

Write short notes on Economic Activity.

Answer:

- Economic activity refers to that activity which is concerned with earning of income and spending of income.

- All the economic activities include those activities related to consumption, production and distribution

- Economic activities are undertaken in order to satisfy various human wants.

- The economic activities constitute the ordinary business of life.

- Economic activities are executed by the rational human beings who pursue to maximise the satisfaction with limited resources.

Question 2.

What is Economic problem ?

Answer:

- Economic problem arises becauses of unlimited wants and imited resources.

- Choice in the context of multiplicity of wants and limited resources constitute the basic economic problem.

- Economic problem emerges because of scarce resources having alternative uses for which choice is to be made.

- Problem relating to allocation of resources, production of goods and distribution of goods also constitute economic problem.

- Problem on the attainment of economic growth also forms the component of economic problem.

Question 3.

Describe Wealth Definition.

Answer:

- Adam Smith, the father of economics formulated the wealth definition of economics

- It is considered to be the first systematic definition of economics

- According to Adam Smith, economics is a ‘Science of Wealth’ and gives emphasis on material wealth.

- It deals with the acquisition of wealth, accumulation of wealth and spending of wealth.

- Thus, Wealth definition deals with the consumption, production and distribution.

Question 4.

Describe Welfare definition.

Answer:

- The welfare definition has been enunciated by Alfred Marshall in his book “Principle s of economics” published in 1890.

- According to Marshall, “Economics is a study of mankind in the ordinary business of life; it examines that part of individual and social action which is closely connected with the attainment and the use of material requisites of well being.”

- Marshall gave primary place to man and secondary to wealth.

- According to Marshall, economics deals with the material welfare.

- Marshall’s definition, thus, classifies the economic activities into material welfare and non-material welfare.

Question 5.

Describe Robbins definitio.

Answer:

- Lionel Robbins formulated a definition which is called “Scarcity definition.”

- According to him, “Economics is the science which studies the human behaviour as a relationship between ends and scarce means which have alternative uses.”

- Choice in the context of satisfaction of multiple wants and scarcity of resources form the basis of this definition.

- Robbins definition deals with the unlimited wants, limited resources having altmative uses and choice for the satisfaction of wants in order of intensity.

- Robbins definition is more analytical, comprehensive and treats economics as a positive science.

Question 6.

Central Problems of Economics.

Answer:

The origin of the economic problem is in scarcity of resources. Multiplicity of ends forces on us the problem of choice among the ends so that the most intense among them are satisfied now. If there were only a single end, the problem of how to use the means would be a technological problem. Solution of a technical problem requires knowledge solely of engineering and physical sciences. Solving an economic problem involves value judgements, for such a problem inevitably involves the calculation of how much of one goal has to be sacrificed to attain a particular increment in an other goal. This is known as the Principle of opportunity cost. It tells us the rate at which we have to sacrifice one goal in order to satisfy another goal by a given amount. This principle is very well illustrated by the Production Possibility Curve to study the economic problems.

Question 7.

What do you mean by production possibility curve ?

Answer:

The set of problems facing every economy can be very clearly analysed with the help of what Professor Samuelson called the Production-Possibilities or Boundary Curve. This curve helps us in distinctly showing the relationships among the set of problems/of an economy. The production- possibility curve illustrates three concepts : scarcity, choice and opportunity cost. A production-possibilities curve shows the various combinations of the goods which an economy can produce with given resources and under the given technology.

Group – B

Long Type Questions With Answers

Question 1.

Describe“Wealth Definition” of Economics.

Answer:

Adam Smith is considered as the first economist who has formulated a systematic definition of economics for the first time in his book “An Enquiry into the Nature and Causes of Wealth of Nations” published in 1776. He defined economics “as a Science of Wealth. ” Hence, his definition is universally accepted as. “Wealth definition. ”

According to Adam Smith, all that economics studies is wealth. Economics deals with the acquisition, accumulation and utilisation of wealth. It looks into the process of production and consumption of wealth.

Features : The “Wealth definition of economics as pronounced by Adam Smith contains the following features:

- Study of Wealth : Adam Smith’s Wealth definition is the study of wealth alone, Hence, it deals with those activities which are related to production, consumption, exchange and distribution.

- Considers only material commodities : Smith’s definition categorically emphasises on only material commodities. Economics, according to Adam Smith, constitutes only material commodities. These are called wealth according to Adam Smith’s definition. As such, this definition ignores non-matrial goods like services of all types, free goods like air, water etc.

- Deals with causes of Wealth : In Wealth definition, it is described that economics studies the causes of wealth accumulation. To increase wealth, production of material goods will have to be stepped up.

- Much emphasis on Wealth: In this definition, wealth is considered to be the sole factors. The main aim of the political economy is to increase the riches (wealth) of the economy.

MERITS :

- Adam Smith’s definition is the first systematic definition of economics which separates economics from politics. This makes economics as an independent subject.

- The Wealth definition of Adam Smith seeks to look into the possible causes which lead to increase the wealth.

- This definition signifies the material goods (material wealth) which are scarce.

- This definition dictates the nature of an economic man who pursues to achieve his needs to the maximum.

DEMERITS :

(i) Gives much emphasis to wealth : Adam Smith’s defintion gives too much emphasis to wealth. Only wealth is treated to be the most significant factor which is even more important than man. Wealth occupies a primary place whereas man occupies secondary place. Thus, definition itself restricts the scope of economics by giving much importance to wealth.

(ii) Provides restricted meaning of wealth: This definition provides a restricted meaning of wealth by considering only material commodities (material wealth). Non-material goods like services of all types are ignored though these services constitute a part of wealth in modern days. Thus, by restricting the wealth to material goods only, this definition has narrowed the scope of economics.

(iii) Ignores wealfare : The concept of welfare which is a significant and long cherished concept has been outrightly ignored by Adam Smith. This definition has not given importance to the economic welfare. It emphasises only on the accumulation of wealth but pays no attention to the equitable distribution of wealth and its uses for the welfare of the society.

(iv) Concept of Economic man : This definition is based on the concept of economic man who works for. Selfish ends alone and not found in real life. But in realism, man’s activities are influenced by moral, social and religious factors.

(v) Ignores problem of Scarcity and Choice : This definition does not make any discussion on the problem of scarcity and choice which are two common concepts to be discussed. Besides, this definition is ambiguous and static in nature Critics like Carlyle, Ruskin and others criticised Adam Smith for his definition and treats economics as a “Dismal Science.” Above all, Wealth definition given by Adam Smith is narrow, controversial and unscientific

![]()

Question 2.

“Economics is a Science of Chocie” Discuss this view in the context of Robbins’ definition of Economics.

Answer:

Lionel Robbins, an eminent English economist enunciated a comprehensive definition on economics. The imperfections and inadequacies of previous definitions inspired him to advocate an analytical definition. In his words, economics is the science which studies the human behaviour as a relationship between ends and scarce means which have alternative uses “Robbins raised economics to a dignified status. In his book “Nature and Significance of Economic Science (1932)” he discussed on the several universal facts with following elements.

ELEMENTS:

- Unlimited wants

- Limited scarce resources.

- Alternative uses of resources.

- Different intensity of wants.

- Problem of choice

1. Unlimited wants : Robbins calls wants as the ends. These ends or wants are numerous, limitless and numberless. When one wants is satisfied, another wants takes its place. Thus, it contended that the human beings confront with the multiplicity of wants. So it is impossible to satisfy all of the wants of human beings.

2. Limited (scarce) resources : In Robbins definition, the term ‘means’ indicate resources. Resources are those things which can satisfy human wants directly or indirectly. But the resources are scarce in the sense that these goods have limited supply in relation to its demand. So the human beings fail to satisfy all of his wants and are compelled to postpone the satisfaction of less urgent wants. The relative scarcity of the resources poses economic problem. So, economics is termed as a Science of Scarcity.

3. Alternative uses of the resources : Prof. Robbins reveals the alternative uses of the resources in his difinition. It implies that these resources can be put into alternative uses. For example, – coal has several uses. This leads to create an economic problem in the allocation of these limited resources.

4. Different intensity of wants : It is derived from the definition that all the wants are not equally important or urgent. It means wants are of different intensity. Some wants are more urgent than other. Thus, a man is forced to make a choice of wants. So Economics, according to Robbins is a Science of Choice.

5. Problem of Choice : Unlimited wants, limited resources and alternative uses of resources create an economic problem. Every man confronts with scarcity of resources. Hence, he is forced to make a choice of wants in his allocation of resources. This problem is the central problem of economics.

MERITS :

Robbins definition is comprehensive and scientific in out look. This definition is superior to wealth and welfare definition and hence is universally appreciated. The major merits of Robbins definition are as follows :

- An analytical definition : Robbins definition is an analytical definition. He provides the reasons for the study of economic problems.

- A universal definition : Robbins definition is universal in nature. It deals with common problems arising out of unlimited wants and limited resources. So it is applicable everywhere.

- More comprehensive definition: Robbins definition combines human behaviour with the choice between ends and scarce means. So this definition has wider scope than other definition.

DEMERITS :

Though Robbins definition is logical and scientific yet it suffers from several demerits.

(i) Self contradictory : Robbins has contradicted himself by his two views about choice between ends, hi the first place, he contends that Economics is the Science of choice These two contentions are mutually contradictory.

(ii) Concept of Welfare : Robbins’ definition has also hidden concept of welfare. According to Robbins, Economics deals with the choice between ends and means. It implies that there is human welfare to solve this problem. Thus, the idea of welfare is very much in Robbins definition.

(iii) Narrow definition : Another drawback of Robbins definition is that it only deals with the problem of choice. But in modem days, the allocation of resources is not the only problem. Rather, there are other problems like distribution of national income, employment, regional development which are ignored in Robbins definition.

However, Robbins definition is unique and has practical validity. It is a comprehensive definition that touches different aspects of Economics ‘

Question 3.

Explain Marshall’s definition of Economics.

Answer:

Alfred Marshall, an eminent British economist has enunciated a definition of economics in his masterpiece “Principles of Economics” published in 1890. Being dissatisfied with the definition given by Adam Smith, Marshall tries to interprete Economics as a Science of Welfare. Hence, Marshall’s definition is otherwise called “Welfare definition”. In his definition, Marshall emphasised on human welfare than wealth. According to him, wealth is a means to satisty human wants but not an end in itself.

Marshall’s definition reads as ‘‘Economics is a study of mankind in the ordinary business of life. It examines that part of individual and social action which is most closely connected with the attainment and with the use of material requisites of well-being ”

Features :

1. A study of mankind : Economics studies the economic activities of man. Man performs many types of activities. They are social, religious and economics. Economics is the study of economic activities which are concerned with the economic activities of man.

2. Ordinary business of life : Every man works mostly to earn wealth and spends his earning to get maximum satisfaction out of it. This is the activity of an ordinary man. Economics studies only ordinary man not extra ordinary people like Sadhus and Santhas etc.

3. Study of Individual & Social action: Economics studies the personal and social activities of man which are concerned with his material welfare. It is a study of the individuals on the one hand and social organisation of economic activities on the other.

4. Study of material welfare : The main emphasis of this definition is on material welfare. This is the major difference of this definition from the definition given by Adam Smith. One must note that economics is a subject which studies the material welfare of man. The study of non material welfare is ignored in his definition.

5. Normative Scieence : According to this definition, economics is the study of the causes affecting material welfare It is therefore a social science. Economics doesnot only concern with the material means; it studies the related activities which of course concern with wealth.

Merits :

1. A classificatory Definition : Marshall’s definition classifies the economic activities of man into two types: (i) Material welfare, (2) Non-material welfare. Similliarly, men are classified as ordinary and extraordinary. Economic activites are classified as individual and social. Thus Marshall’s definition has served to put economics as a class by itself, distinguished from other sciences.

2. Avoids criticism made against Adam Smith : This definition emphasises man and his welfare.lt mentions wealth later on – Prof. Pigou compared economics with the science of medicine. He regarded it as an instrument of the material welfare of mankind. Thus, economics is no more a dismal science.

3. Clear about the Nature of Economics : This definition tells that economics is a social science. It is not a pure science. It is also not an art. It is one among the social sciences.

4. Clear on the scope of Economics : The definition is also having the merit of laying down the scope of economics clearly. It studies only the material activities of man. It is concerned with the ordinary men not extraordinary men.

Criticism:

1. Study of all types of economic activity of men: Marshall’s definition restricted economics to the study of man in the ordinary business of life. According to Robbins, all men have economic problem. This problem is of limited resources and comparatively much more ends or wants. This problem may be called the problem of scarcity. All men, whether rich or poor, are faced by this problem. Therefore, economics studies all men, whether rich or poor.

2. Restricts the scope of Economics : In Robbin,s view, this definition has limited the scope of economics to the study of material goods only which promote material welfare. But there are non-material services of a singer, a doctor, a teacher or a lawyer which have economic value. Thus, the scope of economics is restricted

3. Economics as pure science : The definition based on material welfare tends to show that economics is a social science. This idea in Robbin’s view, is wrong. Economics is not a social science simply because it studies human beings. It may at best be called a human science. It is a pure science like Physics, Chemistry because it has universally applicable laws.

4. The definition is not analytical: This definition is only classificatory in nature,It doesnot tells us the central problem of economics. In Robbins’ view, the definition of economics must be related to a scientific analyscis of economic activities.

5. Economics is a positive Science: Robbins also criticises the Marshallian definition for its normative character. In Robbins’ view, economics is entirely neutral between ends as every positive science is. The study of ends is outside of its scope. An economist does not study the nature of norms.

6. Impractical: This definition is impractical. The material welfare definition assumes that it is possible to divide a man’s activities in to material and non- material, economic and non-economic. In practice, there is no such clearcut distinction between economic and non economic activities. Therefore, the definition is not practical.

![]()

Question 4.

Make comparative analysis between Robbins’ and Marshall’s definitions of Economics.

Answer:

Alfred Marshall and Lionel Robbins propounded two different and separate definitions of economics. Both the formulations bear different aspects of economics. Marshall’s welfare definition and Robbins scarcity definition are enunciated during different periods. But the detailed analysis of the two theme observed certain similarities and dismilarities in their respective contents. So it is not justified to derive a hasty conclusion that these two definitions are completely different from each other.These similarities between the two definitions of economics are discussed below :

Similarities :

1. Wealth and Scarce means : In Marshallian framework, the term wealth is used in form of materal welfare. In Scarcity definition, Lionel Robbins has introduced ‘scarce means’ which simply denotes wealth. It is only the change of words to express and emphasise the wealth in both the definitions. Thus, these two definitions are similar in this respect.

2. Primary place to man : Alfred Marshall’s & Lionel Robbins have given much emphasis on the study of man. Marshall studied wealth for human welfare and Robbins’ described human behaviour as a relationship between ends and scarce means which have alternative uses. Furthermore, Marshall also interpretes that it is on the one side a study of wealth and on the other and more important is the study of a man. Thus, both the definitions aim at the study of human beings.

3. Rational behaviour of man : The comprehensive analysis of both the definitions reveals that both presumes rational man for their study. These two definitions are based on rational behaviour of man. In Marshallian analysis, it tells that man always pursues to maximise his welfare whereas in Robbins language, man tries to maximise his satisfaction. In this context, both the definitions are construed as similar.

Dissimilarities:

In spite of the above mentioned similarities, these two definitions contain certain different concepts. There observed certain fundamental differences between the two definitions.The important distinctions between the two are mentioned below.

1. Distinction between social and human science: According to Marshall and his disciples, economics is viewed as a social science. It studies rational, ordinary social human beings. In Robbins’ view, economics is viewed as human science associated with the economic activities of ordinary and extraordinary men. Every man confronts with economic problem.

2. Distinction between economic and non-economic activities : In Marshallian version, economic activities refer to those activities which are concerned with material commodities promoting material welfare. Robbins’language, all those economic activities the problem of valuation. Thus, Robbins definition is more comprehensive as it includes both the material and non material goods

3. Normative & Positive science: In welfare definition, Marshall clearly describes economics as a normative science. Because it values the welfare of human beings. In Robbins’ version, economics is a positive science.Thus, there lies the difference between the two.

4. Classification and Analytical definition : Marshall’s definition is classificatory in nature because it puts economics as a subject as it is separated from other social sciences. He delimits the subject matter of economics to material activities leading to material welfare. On the otherhand, Robbins submits an analytical definition which concentrates on the basic economic problem.

5. Difference regarding man and his welfare: Marshall’s definition gives much stress on man whereas Robbins’ definition emphasises on the economic problem. From the above analysis, it is presumed that though both the definitions contain some common concepts yet there observed significant differences between the two.

Question 5.

What is the scope of Economics ?

Answer:

By scope of economics, we mean the area of its study or the extent of its study. It is essential to know the boundaries of the study of economics for scientific analysis of the subject In the scope of economics, we discuss its boundaries. Scope of economics answers mainly the following three questions:

1. What is the subject matter of economics ?

2. What is the nature of economics ?

3. What are the limitations of economics ?

Now we will study in detail the answers to these three questions.

Subject Matter of Economics

Subject matter of economics is a controversial subject. That is why Mrs. Barbara Wooton said, “Whenever six economists are gathered, there are seven opinions.” The classical economists like Adam Smith, J.S. Mill, David Ricardo, LB. Say regarded economics as a science which studied wealth. They considered only material goods as wealth. And wealth formed the subject matter of economics. The philosophers of that time criticized this view regarding the subject matter of economics. Marshall removed the defects of the classical view. He regarded economics as a social science studying all those human activities which are related to material welfare. Prof. Robbins found faults with Marshall’s view. So he gave his own opinion and widened the scope of economics, He made economics a science studying all those activities which are related to scarce means in relation to unlimited wants. Thus, according to Prof. Robbins, the problems of valuation and choice are studied in economics.

The scope of economics is very vast. In economics, we study the circular flow of efforts made to satisfy wants and the resulting satisfaction from these efforts.

The economic circle, given on below shows that man has several wants.. In order to satisfy his wants, he makes efforts and thus produces goods and services. From the consumption of these goods and services, he gets satisfaction. Another feature of wants is that when a particular want is satisfied, another want takes its place. So this circular flow goes on as long as a man is alive. It should be borne in mind that wants are of two types: (i) Natural wants, (ii) Artificial wants. Natural wants are those wants which are satisfied by the free gifts of nature like wind, water, heat etc. We do not have to make any effort to get these goods and services. Such wants are not studied in economics.

Artificial wants are satisfied with the man made goods and services like .cloth, food, services of a doctor, etc. Thus we have to make efforts to satisfy them. Artificial wants result from the development of civilisation. They are wants of food, cloth, etc. Only artificial wants form the subject matter of economics.

The study of wants efforts satisfaction is divided into various sections of study. They are : consumption, production, exchange, distribution, public finance and international trade. In consumption, the laws concerning human wants are studied. For example, law of diminishing marginal utility, law of equimarginal utility, etc. In production, we study the means of production and the laws of production. In exchange the price determination through the forces of demand and supply is studied.

We know that production is the result of the combined efforts of the four factors of production which are land, labour, capital, organisation and the entrepreneur. So production is divided among the four factors of production. This division is studied in the distribution section of economics. The last section of the study of economics is public finance and international trade.

According to Chapman, “Economics is that branch of knowledge which studies the consumption, production, exchange and distribution of wealth.”

Peterson said, “Economics is a study of the processes by which goods and services are produced exchanged and consumed.”

Modem economists say that in economics we study the consumer’s equilibrium, producer’s equilibrium, commodity price determination and factor pricing. Both micro and macro types of economic activities are studied in economics. Static as well as dynamic economic activities come under the study of economics.

Now we can conclude that all economic problems, economic policies and economic laws which are concerned with economic activities and human welfare are included in the subject matter of economics. ‘

Question 6.

What are the central economic problems ?

Answer:

The subject matter of economics is concerned with the rational management or optional allocation of scarce economic resources among the alternative uses so that a consumer (individual) can maximize his satisfaction or a producer (entrepreneur) can maximize his profit (output) & economic as a whole can maximize social welfare. It is a fact that economic system is complex as numerous economic agents pursue & prefer to make choices & guided by incentives. In addition to this, the economic activities undertaken by these economic agents are also numerous which & in to all these make the economic system complex.

Every economy has to solve the basic universal economic problem of allocating scarce resources among competing ends. Professor Frank H. Knight pointed out in his book Economic Organisation that the economic problem maybe sub-divided into five interrelated problems. Every society has to devise its methods of solving these five distinct though interrelated problems. These problems are:

- fixing standards (What to produce ?)

- organising production (How to produce ?)

- distributing the product (how to distribute or whom to produce ?)

- providing for economic maintenance and progress (or how to ensure economic growth?)

- adjusting consumption to production over short periods (how to ration the limited supplies).

Being confronted with the above fundamental economic problems, the functions of an economy is concentrated on the rational solution of these problem which originate due to scarcity of resources and competing ends. Solving an economic problem value judgements, for such a problem inevitably involves the calculation of one goal which is to be for gone to achieve a particular increment in an other goal. This is known as the “Principle of Opportunity Cost”. Applying this concept, the economy functions to solve the above problems.

1. Determinng What to Produce : Given the economy’s resource endowments, the first function of an economy aims at determining the composition of output. In a free economy the forces determining the composition of output can be classified into two types : (1) the technology (or input-output co-efficients) which determines the relative cost of each product, and (2) consumers ’ tastes and preferences which determine the relative prices of different goods. Since resources at the disposal of every economy are limited, the allocation of given resources has to be done according to the technology available for transforming the resources into the desired goods which, in turn, depends upon the tastes of the consumers. In a free enterprise economy, the composition of output is determined by the equality of the marginal rate of transformation of a good A into good Y with the marginal rate of substitution of the community for the two goods.

2. Determining How to Produce: Once composition of output is determined by consumers tastes and preferences, the organisation of production is taken up by the business firms. The business firms decide on the allocation of resources and the methods of production keeping the relative prices of the resources and technique of production in vient. The firms would try to attain productive efficiency by combining resources to obtain the given output at least cost and selling the produced output in the most profitable way. Thus, a free enterprise economy, depending upon the price mechanism, takes the two decisions of what to produce and how to produce at the same time. In the process, each resource is used according to its relative abundance or scarcity among different uses.

3. Distribution of National Product (Determining whom to produce) : Decision about the distribution of the national product among the members of the community has two aspects. First, the economy has to determine the relative sizes of the shares to be received by each household. Second, the economy has to determine the bundles of goods and services available to each household. The resource- owning households sell their resources for production and, with the incomes so earned, demand the goods and services produced by the producing firms. The resource owners-sell their services at the highest obtainable prices for them. At the same time, the households try to purchase the satisfaction-maximising bundles of goods and services available through spending their incomes. In this way, the decisions about production and distribution are co-ordinated and made consistent.

4. Rationing of Available Supplies : Price mechanism in a free-enterprise economy also decides how the available supplies of consumers goods would be rationed to consumers over the short run. Some commodities may be in shortage for some time to come. For example, sugar or vanaspati ghee supply may be short of demand which leads to rise in their prices. The consumers adjust their demands for these commodities according to their tastes and incomes in view of the high prices of these commodities. As the seasonal supplies of these commodities get depleted, their prices rise further to attain the limited supplies among prospective consumers.

5. Economic Maintenance and Progress (Economic Growth) : This function of an economic system has three aspects :

(a) maintaining the economy’s productive powers in the face of increasing population;

(b) maintaining the production system through replacement of capital goods which are depreciating in the process of production;

(c) improving the technical processes so as to enhance the nation’s productive power and step up the rate of growth of the national product.

According to Frank H. Knight, this function of maintaining the economic system cuts across all the other functions. It implies stabilising the rate of investment to provide for replacement and growth of capital stock on the one hand and improving the productivity of resources within the economy through technological progress. In a free enterprise economy, this function is performed by individual firms, the government providing the needed infrastructure to facilitate their work.

Question 7.

Discuss the concept of Production possibility curve.

Answer:

The production-possibility curve illustrates three concepts : scarcity, choice and opportunity cost. Let us take up the problem of choice betw een Goods X and Goods Y meant for. If we have full employment of resources and we want to produce more X, then we must produce less of all other goods, thereby reducing the quantity of goods (Y) available to satisfy the needs. The country must make a choice of the combination of X and Y. More X mean less for consumption and vice versa. The opportunity cost of more X is shown by the amount of goods Y forgone in greater production of goods X.

Choice & concept of Opportunity cost: The following table shows the combinations of X and Y for a country which has a choice of production between butter and guns. Given the research and technology in our hypothetical economy, we can produce only so much X and so many Y. The table given below gives the combination of Y and X which can be produced assuming that’ only these two outputs are produced. Combination A shows no X, all Y, On the other extreme, combination F shows all X, no Y. Combinations B to E show that in order to have more Y, we must have less of X. This is the principle of opportunity cost. The opportunity cost of getting five lakh quintals of X in combination B, for example, is three Lakh Y which have to be given up in moving from combination A to combination B.

![]()

TABLE

Production Possibilities

| Combinations | X

(lakh quintals) |

Y

(lakhs) |

| A | 0 | 40 |

| B | 5 | 37 |

| C | 1o | 32 |

| D | 15 | 25 |

| E | 20 | 15 |

| F | 25 | 0 |

The concepts of scarcity, choice and opportunity cost become even more illuminating if we translate the table of production possibilities into a graph, which we call a production-possibilities curve.

A production-possibilities curve shows the various combinations of the goods which an economy can produce with given resources and under the given technology. Figure reveals a Production-Possibility curve from the point A to F. On the horizontal & axis, the quantity of goods X produced is measured while the vertical Y-axis measures the quantity of all other goods, that is, goods Y).

We plot-all those combinations of X goods and Y goods which can be produced if all the resources are fully employed. The points A, E, B, Fare the points on the production possibility curve AF. This curve separates the combinations of the goods obtainable from the use of given resources from those which are not attainable. Points in side the boundary such as C show the combination of and goods xy which are attainable. Points outside the boundary such as D show combinations which are not attainable because there are not enough resources to produce them. Points on the production- possibility boundary such as E and B are just obtainable. These are the combinations which can be produced only if we use all the available resources. The fact that there are combinations which are not attainable in the diagram shows that there is scarcity of resources and we are thereby forced to make a choice between more or less of one type of goods or the other.

The downward slope of the production possibility curve shows that there is an opportunity cost of producing more of goods X or more of goods Y the opportunity cost being measured by the quantity forgone of the other type of commodity. Thus if we go from point E to point B we are reallocating resources out of production of Y and into production of X as a result of which the quantity of production of X rises from OQ to OS while that ofY production of falls from OP to OR. Thus the opportunity cost of getting QS more of goods X produced is PR goods y sacrificed. This illustrates the problem of allocation of resources in the economy.

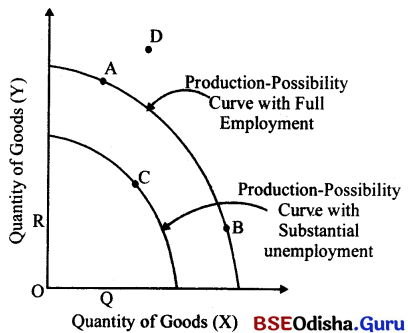

It is, of course, always possible that actual production in the economy takes place “at some point inside the production-possibility curve. This is possible either because some of its resources are lying idle or because its resources are being used inefficiently in production; Most of the world’s developed “economies are found to operate on or near about the production- possibility curve in normal times. Almost all the world’s less developed countries produce well inside the production- possibility curve simply because they are unable to manage full employment of their resources. The point C in Fig. is one such point which shows considerable unemployment of the economy’s resources.

The higher the proportion of resources unemployed, the closer will the actual point of production be to the origin.

If the economy is at some point inside the boundary such as point C, then it must be enquired as to why the available resources are not being fully utilised. If the reasons are not being fully utilised because of imperfections in the market mechanism, then these imperfections must be removed. On the other hand, if the un-employed resources are idle because of lack of some complementary factors, then these can be imported to employ these resources. Or the structure of production in the economy has to be changed in order to use all the resources in the country and that too efficiently.

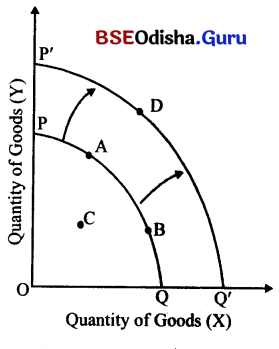

Finally, let us deal with the question of economic growth. A country can push its production- possibilities curve outwards by increasing the economy’s capacity to produce goods over a period of time. For example. Fig. shows the shift of the curve PQ to the position P’Q’ through increased productive capacity which is measured as PP’ of goods Y or QQ’ of goods Y. In this case, if the economy remains on the product ion- possibility boundary, it will be possible to increase the production of all goods over time, moving, for example, from point A to point D. It is clear from this analysis that if we want to increase the production of all goods in the economy, it is necessary to take one of the two steps possible :

(1) If the economy is operating at a point inside the production-possibility curve, then the economy can be made to move on to a point on the curve itself, for example, from point C to point B. This can be done by improving the efficiency of production.

(2) If the economy is already operating on the boundary, then it is necessary to take steps which will move the boundary itself outwards so that production can expand. Shift of the production-possibility curve to the right is possible only through economic growth.

The first method consists of a set of policies based on macroeconomics. The second method is based on what has come to be called economics of growth.

Group – C

Objective type Questions with Answers

I. Multiple Choice Questions with Answers :

Question 1.

Who is the father of Economics ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Robbins

Answer:

(ii) Adam Smith

Question 2.

Who has propounded the Welfare definition of Economics ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Robbins

Answer:

(iii) Alfred Marshal

![]()

Question 3.

Who told, “Economics is a Science of Choice” ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Lionel Robbins

Answer:

(iv) Lionel Robbins

Question 4.

Who told, “Economics is a Science of Welath” ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Lionel Robbins

Answer:

(ii) Adam Smith

Question 5.

Who has termed Economics as a Science of Material Welfare ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Lionel Robbins

Answer:

(iii) Alfred Marshal

Question 6.

Who has Popularised the scarcity definition of Economics ?

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Lionel Robbins

Answer:

(iv) Lionel Robbins

Question 7.

What Constitutes the subject matter of Economics ?

(i) Wants

(ii) Efforts

(iii) Satisfaction

(iv) All of the above

Answer:

(iv) All of the above

Question 8.

Which is the basic components of Scarcity definition ?

(i) Wants are unlimited

(ii) Resources are limited

(iii) Resources are alternatively used

(iv) All of the above

Answer:

(iv) All of the above

Question 9.

Scarcity of resources and choice are very much present in the definition of

(i) J.M. Keynes

(ii) Adam Smith

(iii) Alfred Marshal

(iv) Lionel Robbins

Answer:

(iv) Lionel Robbins

Question 10.

Which definition studies the ordinary business of life ?

(i) Welfare definition of Marshall

(ii) Adam Smith’s Wealth definition

(iii) Lionel Robbin’s Scarcity definition

(iv) None of the above

Answer:

(i) Welfare definition of Marshall

II. Fill in the blanks :

1. The term “Economics” is originally derived from Greek words _____

Answer:

“Oikis”

Question 2.

“Oikis” means _____

Answer:

“Household”

Question 3.

The term “economics” was first of all used by _____

Answer:

Dr. Alfred Marshall

Question 4.

The Principle of Economics” published in 1890 was written by _____

Answer:

Alfred Marshall

Question 5.

_____ had given Wealth Definition of economics

Answer:

Adam Smith

Question 6.

_____ is the exponent of Welfare Definition of Economics.

Answer:

Alfred Marshall

Question 7.

The Scarcity Definition of Economics is given by _____

Answer:

Lionel Robbins

Question 8.

The Name of the book written by Adam Smith was _____

Answer:

“An Enquiry into the Nature and Causes of wealth of Nations”

Question 9.

According to Adam Smith Economics is the study of _____

Answer:

Wealth.

Question 10.

According to Marshall Economics is the study of _____

Answer:

Mankind.

Question 11.

Human wants are _____ and Resources are _____

Answer:

unlimited, limited

Question 12.

The scarcity definition has been enunciated by _____

Answer:

Lionel Robbins

Question 13.

_____ arises beacause of unlimited wants and limited resources.

Answer:

Economic Problem

![]()

Question 14.

Wants, effort _____ constitute the subject matter of economics

Answer:

Satisfaction

Question 15.

The production possibility curve slopes _____to the Right:

Answer:

Downwards

Question 16.

The production possibility curve is _____ the origin

Answer:

Concave

III. Correct the Sentences :

Question 1.

Economic problem arises because of limited resources & limited wants.

Answer:

Incorrect:

Correct: Economic problem arises becaues of limited resources & unlimited wants.

Question 2.

Economics has been derived from latin words.,

Answer:

Incorrect:

Correct: Economics has been derived from Greek words.

Question 3.

Marshall formulated the first systematic definiton of Economics

Answer:

Incorrect:

Correct: Adam Smith formulated the first systematic definition of economics.

Question 4.

Marshall defined economics as a “Science of Wealth.

Answer:

Incorrect:

Correct: Adam Smith defined economics as a “Science of Wealth.”

Question 5.

Lionel Robbins is the Father of Economics.

Answer:

Incorrect :

Correct: Adam Smith is the Father of Economics.

Question 6.

Adam Smith gave much emphasis to material welfare.

Answer:

Incorrect

Correct Marshall gave much emphasis to material welfare.

Question 7.

Adam Smith formulated “ Welfare definition” of economics.

Answer:

Incorrect

Correct Alfred Marshall formulated “Wealfare defintion of economics.

Question 8.

Alfred Marshall wrote the book “Principles of economics”.

Answer:

Correct

Question 9.

In Marshall’s definition wealth occupies a primary place.

Answer:

Incorrect

Correct In Marshall definition man occupies a primary place.

Question 10.

In Marshall’s definition the term welfare includes only material welfare.

Answer:

Correct

Question 11.

Lionel Robbins’ defined economics a Science of Choice.

Answer:

Correct

Question 12.

Marshall enunciated “Scarcity definition” of economics.

Answer:

Incorrect

Correct Lionel Robbins’ enunciated “Scarcity definition of economics.’

Question 13.

Want are limited but resoures are unlimited.

Answer:

Incorrect

Correct. Wants are unlimited but resoures are limited.

Question 14.

Scarcity means excess of supply over demand.

Answer:

Incorrect

Correct. Scarcity means excess of demand over supply

Question 15.

Resources are of single use.

Answer:

Incorrect.

Correct. Resources are of alternative uses.

Question 16.

Choice in Robbins’ definition refer to choice of resources.

Answer:

Incorrect.

Correct. Choice in Robbins’ definition refer to choice of satisfaction of present wants over future. ‘

Question 17.

The Production possibility curve is upward sloping.

Answer:

Incorrect

Correct: The Production possibility curve is downward sloping

Question 18.

The Production possibility curve is concave to the origin.

Answer:

Correct: The Production possibility curve is concave to the origin.

![]()

Question 19.

Scarcity of resources is the starting point of economics.

Answer:

Incorrect

Correct: Human wants is the starting point of economics.

Question 20.

Wants, efforts and Satisfaction constitutes the scope of economics.

Answer:

Incorrect

Correct: Wants, efforts and Satisfaction constitutes the Subject matter of economics.

IV. Answer the following questions in One word/One Sentence :

Question 1.

What is meant by Economics ?

Answer:

Economics studies all the human activities concerning wealth. It studies the production, consumption, exchange and distribution of wealth.

Question 2.

What is the basic economic problem ?

Answer:

The basic problem in Economics is the satisfaction of wants which involves choice. The choice in the context of multiplicity of wants and limited resources poses to be the basic economic problem.

Question 3.

Why do economic problems arise ?

Answer:

Economic problems arise on account of scarcity of resources and unlimited nature of human wants.

Question 4.

From which word the term ‘Economics’ has been derived ?

Answer:

Economics has been derived from two Greek terms like “Oikos” which means household and “Nemein” which means‘management.’

Question 5.

What is Economics ?

Answer:

Economics is a social science which deals with consumption, production, distribution and exchange of wealth.

Question 6.

What is subject matter of Economics ?

Answer:

Wants, efforts and satisfaction constitute the subject matter of economics.

Question 7.

What is basic economic problem ?

Answer:

Unlimited wants, scarcity of resources and choice for satisfaction of wants constitute the basic economic problem.

Question 8.

Who is the first economist to use the term “Economics” ?

Answer:

Alfred Marshall is the first economist who used the term “Economics” in his book “Principle of Economics” in 1890.

Question 9.

What are the economic activities ?

Answer:

Economic activities refer to those activitis which are concerned with earning of income and spending of income.

Question 10.

Who is the “Father of Economics” ?

Answer:

Adam Smith is the “Father of Economics.”

Question 11.

Which book is the first systematic book on Economics ?

Answer:

“An Enquiry into the Nature and Causes of the Wealth of Nations” is the first book written by Adam Smith in a systematic manner.

Question 12.

What is the name of the book written by Adam Smith ?

Answer:

“An Enquiry into thne Nature and the Causes of Wealth of Nations” is wirtten by Adam Smith.

Question 13.

Who formulated the Wealth definition ?

Answer:

Adam Smith formulated Wealth definition.

Question 14.

What is material wealth ?

Answer:

Material wealth refers to all those commodities which are tangible, visible & have exchange value.

Question 15.

What is the name of the books written by Alfred Marshall ?

Answer:

Alfred Marshall wrote a book named “Principles of Economics” in 1890.

Question 16.

Who gave the Welfare definition of Economics ?

Answer:

Alfred Marshall gave the welfare definition of Economics.

Question 17.

Which occupied primary place in Marshall’s definition ?

Answer:

Man occuupies primary place in Marshall’s definition.

Question 18.

Which concept constitutes the sole factor in Marshall’s definition ?

Answer:

Material welfare.

Question 19.

What is material Welfare ?

Answer:

Material welfare refers to acquision and utilisation of material wealth which can promote human welfare.

Question 20.

What is the ordinary business of life ?

Answer:

The ordinary business of life is to earn and to use the material means for the satisfaction of human wants.

Question 21.

What is Robbins’definition ?

Answer:

Robbins’ definition says “Economics is the science which studies the human behaviour as a relationship between ends and scarce means which have alternative uses.”

Question 22.

Who propounded the “Scarcity definition” of Economics” ?

Answer:

Lionel Robbins propounded the “scarcity definition of Economics.”

Question 23.

What do you mean by scarcity ?

Answer:

Scarcity refers to a situation of excess demand in relation to supply.

Question 24.

What do you mean by resources ?

Answer:

Resources are those goods and services which can satisfy human wants directly and indirectly.

Question 25.

What is the nature of resources ?

Answer:

Resources are of alternative uses.

Question 26.

What is the meaning of “Ends” in Robbins’ definition ?

Answer:

In Robbins’definition “ends” means wants.

Question 27.

What do you mean by wants ?

Answer:

The desire for the possession of a commodity is known as wants.

Question 28.

Who said “ Economics is a science of choice” ?

Answer:

Robbins’ said “Economics is a Science of Choice”.