Odisha State Board CHSE Odisha Class 12 Economics Solutions Chapter 6 Cost and Revenue Questions and Answers.

CHSE Odisha 12th Class Economics Chapter 6 Question Answer Cost and Revenue

Group – A

Short type Questions with Answers

I. Answer within Two/Three sentence.

Question 1.

What is the shape of Marginal cost curve ?

Answer:

Marginal cost first falls because of the increasing returns from the factors in which MP of the factor increases. Secondly, marginal cost increases because of the diminishing returns from the factors & hence marginal lost becomes U-shaped.

Question 2.

What is shape of Short-run average cost (SAC) curve ?

Answer:

On account of the emergence of stage of increasing & diminishing returns, the AP of the factor increases & diminishes. This has the impact on the short-run Average cost for which it first falls & then rises & becomes U-shaped.

Question 3.

What, is nature of Average fixed Cost (AFC) with the increase in the level of output ?

Answer:

The total fixed cost is fixed in the short-run irrespective of the level of output. So with the increase in the level of output, the fixed cost per unit of output (AFC) goes on decreasing.

Question 4.

What is the relationship between Marginal cost and Average cost ?

Answer:

As long as MC < AC, AC must be falling & when MC > AC, AC must be rising. So, MC=AC at the minimum point of AC.

Question 5.

What is the nature of Variable Cost ?

Answer:

In the Short-run total fixed cost remains fixed & only the variable cost changes with the change in the level of output. So variable cost is the prime cost.

Question 6.

What is the relationship between average revenue and marginal revenue in perfect Competition ?

Answer:

In perfect competition, the goods are hemogeneous & sold at a uniform price by the large number of buyers & sellers So additional revenue from the extra unit sold (MR) & revenue per unit of output (AR) becomes same.

Question 7.

What is the slope of average revenue curve in Monopoly ?

Answer:

Under monopoly, single seller sells the product having no close substitute & if he wants to sell more, it is to reduce the price & vice-versa. So AR curve slopes downward.

Question 8.

Which revenue reflects price of the goods ?

Answer:

Average Revenue (AR) is the total revenue perunit of output \(\left(\frac{\mathrm{TR}}{\mathrm{q}}\right)\). So it reflects price

![]()

Question 9.

Which cost is called alternative cost ?

Answer:

The opportunity cost of any goods is the best alternative goods that is sacrificed. So it is called alternative Cost.

Question 10.

Which cost is independent of level of output ?

Answer:

Fixed cost is incurred for the use of fixed factors which remain unchanged in the short- run irrespective of the level of output. So fixed cost is independent of level of output.

Question 11.

What is Total cost ?

Answer:

Both fixed factors & variable factors are employed in the production for which fixed costs as well as variable costs are incurred. So total fixed cost & the total variable cost mixed together indicates total cost.

Question 12.

What is the shape of AR curve in under perfect competition ?

Answer:

Under perfect competition, price of goods remains uniform. So AR curve as well as MR curve is equal & horizontal straight line.

Question 13.

What is slope of AR curve under monopoly ?

Answer:

Under monopoly, if sella- wants to sell more, it is to reduce the price & vice-versa. So the AR curve slopes downward from left to right.

II. Answer within Five/Six sentence :

Question 1.

What is Total Revenue (TR) ?

Answer:

Total Revenue refers to the aggregate of income earned by the seller from the sale of his output. It is the sum of all sales, receipts or income of a price per unit multiplied quantity sold. Thus,

TR = P × Q Where P → Price per unit

Q → Output.

Question 2.

What do you mean by Average Revenue (AR) ?

Answer:

Average Revenue refers to the revenue received per unit. It is the per unit revenue received from the sale of one unit of a commodity. AR is calculated by dividing the Total Revenue by total output. Hence, symbolically,

AR = \(\frac{TR}{Q}\) Where Q – Output

AR is equal to price of the commodity.

AR = \(\frac{PQ}{Q}\) = P where P → Price.

Question 3.

Explain the concept Marginal Revenue (MR).

Answer:

Marginal Revenue refers to the net revenue obtained by selling an additional unit of the commodity. In other words, Marginal Revenue is the change in the total revenue which results from the sale of one more or one less unit of output. Thus, Marginal Revenue is the addition made to the total revenue by selling one more unit of the good.

MR = \(\frac{\Delta \mathrm{TR}}{\Delta \mathrm{Q}}\)

MRn = TRn – TRn-1

Question 4.

Explain the relationship between TR, AR and MR.

Answer:

TR goes on rising as long as MR remains positive. TR becomes maximum when MR is zero. TR starts falling when MR becomes negative and when AR falls MR follows AR, but MR falls at a faster rate than AR. When the AR curve goes on falling the MR curve lies below the AR. When AR rises the MR lies above the AR. The position of the MR is determined by the slope of the AR. When the AR curve is convex to the origin the MR curve is farther from the AR curve. When the AR curve is concave the MR curve lies closer to the AR curve.

(A) WRITE SHORT NOTES ON :

Question 5.

Money Cost.

Answer:

Money cost refers to the monetary expenses incurred by the producer to produce a given quantity of a goods. In other words, the cost of production incurred & expressed in terms of money is called money cost. Money cost is otherwise known as “Nominal cost”. It is expressed as sum of payments made to different factors of production in terms of money. Money cost includes wages for labourers, payment for raw materials, interest, taxes etc.

![]()

Question 6.

Accounting Cost.

Answer:

Accounting cost refers to the cost which can be expressed & whose accounts can be maintaned by the accountant. Accounting costs are expressible & hence called explicit cost. These costs are actually paid by the producer for hiring different factors of production. These accounting costs are nothing but the cash payments made to different factor owners such as wage, rent, interest paid in the productive process.

Question 7.

Economic Cost.

Answer:

Economic cost is a broader concept which includes both explicit cost & implicit cost. It takes the direct cost incurred & paid in terms of money to different into account along with the cost arising from land Owned & used by the producer, entrepreneurs self invested capital, self managment etc. Economic cost includes the total cost which covers both the explicit & implicit cost. The net profit is calculated by deducting this economic cost from the total revenue.

Question 8.

Real Cost.

Answer:

Real cost refers to all those efforts, sacrifices, troubles, toils undergone by the factors owners or the members of the society to produce a goods. It is a subjective concept. It also denotes the exertion of all different kinds of labour that are directly or indirectly involved in the production of goods. It is also called social costs’. It can not be meausred quantitatively & hence no monetary reward is paid.

Question 9.

Opportunity Cost.

Answer:

The opportunity cost of anything is the next best alternative that could be produced instead by the same factors or by an equivalent group of factors costing the same amount of money. In other words, the opportunity cost of any good is the next best alternative good that is foregone. For example, a farmer producing wheat in his land can not produce sugar cane simultaneously. So the production of sugar cane is sacrificed. The opportunity cost of producing wheat is the value of sugarcane sacrificed. This opportunity cost is otherwise called transfer cost or alternative cost.

Question 10.

Fixed Cost

Answer:

Fixed costs denote those costs which are incurred for the fixed factors employed in the productive process. Fixed costs remain unchanged irrespective of the level of output. Even at zero level of output, fixed cost is to be borne. The costs incurred towards land or building, plants & machiney insurance charges etc. are included in the category of fixed cost. Fixed costs are otherwise called “Supplementary cost” or indirect cost. It is also called “ overhead cost”.

Question 11.

Variable Cost.

Answer:

Variable costs are those costs which change with the change in the level of output. It increases with the increase in the level of output & decreases with the decrease in the level of output. Variables costs are called “direct cost” & also treated as “prime cost” during the short-run. The wages, the payment for raw materials are the examples of variable costs.

(B) DISTINGUISH BETWEEN

Question 12.

Explicit cost & Implicit Cost.

Answer:

- Explict cost is that cost which is expressible in any form, but implicit cost is inexpressible.

- Explicit cost is actually paid by the producer to hire different factors of production whereas implicit cost includes entrepreneurs self owned & self employed resources for which no payment is actually made.

- Explicit cost can be properly maintained by an accountant but the accounts of implicit cost can not be maintained.

- Gross profit is calculated by deducting only explicit cost from total revenue but net profit is calculated by deducting both implicit & explicit cost.

Question 13.

Money Cost & Real Cost.

Answer:

- Money cost refers to the cost which is paid in terms of money whereas real cost refers to efforts & sacrifices undergone by the factor owners or the members of the society for producing a commodity.

- Money cost is directly borne by the producer but real cost is the “spill over cost” borne by the society as a whole.

- Money cost is incurred through cash payment to factor owners but no real payment is made in respect of real cost.

- Money cost is a quantitative or objective concept but real cost is qualitative or subjective concept.

Question 14.

Fixed cost & Variable Cost.

Answer:

- Fixed costs are those costs incurred for hiring fixed factors like land & building, plant & machinery whereas variable costs are those costs incurred for hiring variable factors like labour, raw materials, fuel etc.

- Fixed costs remain unchanged irrespective of the level of output. It is indepedent of level of output. Variable costs change with the change in the level of output. It depends on the level of output.

- Fixed costs are the supplementaiy or overhead costs that happen only in the short-run but variable costs are the prime cost which happen both in the short-run & in the long-run.

- Fixed cost exist even at zero level of output but variable cost does not appear at zero level of out-put.

Question 15.

Average Cost & Marginal Cost

Answer:

- Average cost is the total cost per unit of output. But marginal cost is the addition made to the total cost for producing one extra unit of good.

- Both average cost & marginal cost are calculated from total cost.

- When average cost is falling, MC < AC

- When average cost is rising, MC > AC

- Marginal cost becomes equal to average cost when average cost is minimum.

Group – B

Long Type Questions With Answers

Question 1.

What are the components of total cost ? How can total cost be derived in the short-run ?

Answer:

Cost of production refers to the total expenditure incurred for producing a given level of output. It is incurred for hiring different factors of production to be employed in the productive process. The concept of cost can be classified on the basis of the time period i.e. short-run & long- run. In traditional theory of cost, cost can be distinguished as short-run costs & long-run costs.

Total cost refers to the aggregate of expenditure incurred towards the various factors of production to produce a given quantity of output. It is the function of output to be produced. It increases or decreases with the increase or decrease in the level of output. In short-run, there are two components of total cost i.e. total fixed cost-(TFC) & total variable cost (TVC). The sum of total fixed cost & total variable cost gives rise to the total cost during short-period. (Mathematically, stated, TG=TFC +TVC.) For the derivation of total cost, these two components must be looked into.

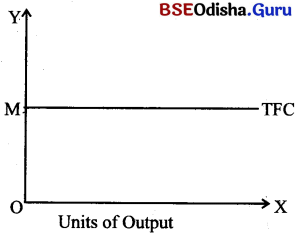

Total Fixed Cost (TFC)

Total fixed cost is the cost incurred for employing fixed factors which are observed to be constant during short-run. Hence, total fixed costs denote to those costs which remain unchanged or constant in the productive process irrespective of the level of output. Thus, total fixed cost is quite independent of level of output. Any change in the level of output does not have any impact on this total fixed cost. Even at zero level of output, total fixed cost is to be borne. These cost are otherwise called overhead or supplementary cost. The cost of building, machinery, land, salaries of the executives etc. are the examples of fixed costs. The total fixed cost curve is a horizontal straight line.

In the figure units of outputs are measured on OX-axis & cost on the OY-axis. TFC is the total fixed cost which is constant (OM) irrespective of the level cost output.

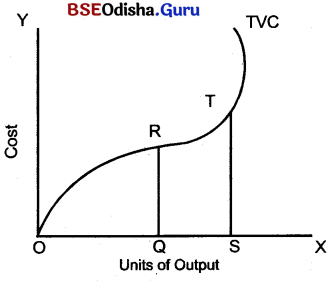

Total Variable Cost-(TVC)

Tota variable costs are those cost which go on changing with the change in the level of output. Any increase in or decrease in level of output causes an increase or decrease in the total variable cost. It is otherwise called prime cost as it is a vital cost concept in the short-run. Expenses towards raw materials, labour power, fuel etc. are the examples of toal variable cost.

In the above figurem units of outputs are measured on OX-axis & cost on OY-axis. For producing OQ amount of output, the variable cost amounts to QR & for higher level of output (OS), it increases to ST. Thus, it is obvious that total variable cost increases with the increase in the level of output & decreases with the decrease in the level of output.

Derivation of TC.

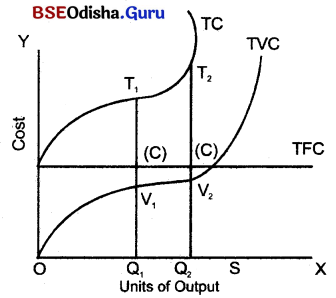

As known total cost is the sum of total fixed cost & total variable cost. This total cost can be numerically derived by summing both these two costs & graphically total cost can be derived through vertical summation of total fixed cost curve & total variable cost curve.

| Units of Output | Total Fixed Cost (Rs.) | Total Variable Cost (in Rs.) | Total Cost (in Rs.) |

| 0 | 10 | 0 | 10 |

| 1 | 10 | 8 | 18 |

| 2 | 10 | 13 | 23 |

| 3 | 10 | 16 | 26 |

| 4 | 10 | 20 | 30 |

| 5 | 10 | 26 | 36 |

| 6 | 10 | 35 | 45 |

| 7 | 10 | 45 | 55 |

The numercial analysis as above presents a break-up of total cost (TC) into total fixed cost (TFC) and total variable cost (TVC). It reveals that TFC remains unchanged (Rs. 10) irrespective of the level of output. But TVC increases with the increase in the level of output. Accordingly total cost being the sum of TFC & TVC increases with the increase-in the level of output. The same notion can be explained with the help of graphical analysis.

The above diagram measures units of output on OX- axis & cost on OY-axis The diagram describes that total fixed cost (TFC) remains constant & hence TFC curve is a horizontal straight line indicating OC amount of total fixed cost. But the total variable cost (TVC) increases with the increase in the level of output & thus TVC curve is inverse – S- shaped. As such TC being the vertical summation of TFC & TVC is represented through TC curve.

The figure also exposes that at OQ1 level of output, the TFC is OC & TVC is Q1V1 At this level, TC is found to be Q1T1, which is obtained by adding TVC (Q1V1) & TFC (OC).

∴ Total cost (TC) at OQ1 level of output = O1V1 + Q1C = Q1T1 Similarly, at higher level of output OQ2, the TFC remains unchanged at OC level as before & TVC increases to Q2V2. AT this level, TC is the sum of TFC (OC) & TVC (O2V2) i.e Q2T2.

∴ TC at OQ2 level of output = Q2V2 + Q2C = Q2T2

In this manner TC is derived in the short-run TC is found to be the aggregate of TFC & TVC.

![]()

Question 2.

Explain Average Cost in the Short-run. How can it be derived ?

Answer:

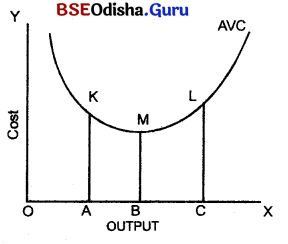

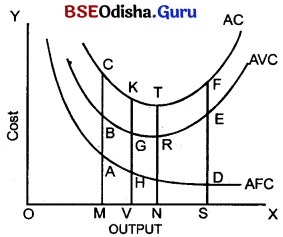

Average cost is the total cost incurred per unit of output. In the short-run, the analysis of average cost can be made by the way of its compnents exist in the short-run. Short-run is a period during which there are two types of costs like Total fixed cost (TFC) & Total variable cost (TVC). So in order to analyse the short-run average cost, there is need of analysing Average fixed cost (AFC) & Average variable cost (AVC).

Average fixed cost (AFC) :

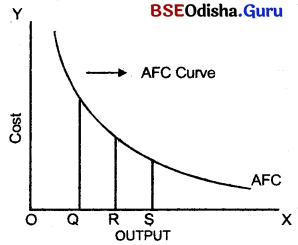

As one of the components of C in the Short-run, Average fixed cost (AFC) can be defined as fixed cost per unit of output (Q). It can be calculated by dividing units output produced (Q) with the i.e. AFC = \(\frac{TFC}{Q}\)

Nature : As total fixed cost is a constant entity in the short-run cost structure, the AFC continuously falls with the increase in the level of output. Thus AFC gradually declines with the increase in the level of output. Hence, AFC curve slopes downward from left to right & takes the shape of rectangular hyperbola. This curve approachs both the axes but does never touch any axis.

In the figure, it is revealed that when the level of output (measure on OX-axis) increases, the cost (measured on OY-axis) falls. At OQ level of output, AFC is found to QA& when output level increases to OR & OS, the A’FC falls to RB & SC respectively. Thus AFC curve approaches both the axes but does not touch any axis.

Average Variable Cost.

Total variable cost incurred per unit of output is called average vriable cost. It can be calculated by dividing quantity of output (Q) produced with the total variable cost (TVC). Symbolically expressed.

AVC = \(\frac{TVC}{Q}\)

Nature :Average variable cost (AVC) at the intial stage diminishes with the increase in the level of output. After a point AVC increases with the increase in the level of output AVC curve takes the shape of‘U’. The nature & shape of AVC is due to the operation of “Law ofVariable Proportions”.

The figure describes that when the output (measured on OX-axis) increases, the average variable cost (AVQ declines. When output level increases from OAto OB, it falls fromAK to BM. At OB level of output, the AVC is minimum at OC level of output, the AVC is found to CL.

Here, output level OA BM < CL

Derivation of AC

Theoretically, short run AC can be derived from the TC which is composed of TFC & TVC TC = TFC + TVC

⇒ \(\frac{TC}{Q}\) = \(\frac{TFC}{Q}\) + \(\frac{TVC}{Q}\)

⇒ AC = AFC + AVC

The derivation of short-run average cost can be numerically & graphically represented.

| Unit of output | TFC (in Rs.) | TVC (in Rs.) | TC (in Rs.) | AFC (in Rs.) | AVC (in Rs) | AC (in Rs.) |

| 1 | 10 | 8 | 18 | 10 | 8 | 18 |

| 2 | 10 | 13 | 23 | 5 | 6.5 | 11.5 |

| 3 | 10 | 16 | 26 | 3.3 | 5.3 | 8.6 |

| 4 | 10 | 20 | 30 | 2.5 | 5 | 7.5 |

| 5 | 10 | 26 | 36 | 2 | 5.2 | 7.2 |

| 6 | 10 | 35 | 45 | 1.66 | 5.83 | 7.49 |

| 7 | 10 | 45 | 55 | 1.42 | 6.42 | 7.84 |

| 8 | 10 | 60 | 70 | 1.25 | 7.5 | 8.75 |

The above analysis indicates that AC is the sum of AFC & AVC. Secondly, it shows that the AFC goes on falling with the increase in the level of output. Thridly. the AVC is found to be falling upto the production of 5th unit of output & afterwards it goes on increasing with the increase in the level of output. On this basis, AC also falls upto the production of 5th unit then increases with the level of output.

GRAPHICAL ANALYSIS

The same principle can be reflected with the help the graph.

The figure reflects the shapes of AFC, AVC & AC curves. Primarily, the AFC curve gradually diminishes with the increase in the level of output. AFC curve takes the shape of a rectangular hyperbola. The AVC curve is U-shaped. At first, it goes on diminishing upto a point & then increases. The minimum point of AVC curve is shown as point ‘G’ in the figure. The AVC curve is thus U- shaped. It goes on diminishing upto the production on the level of output & the increases with the increases in the level of output.

As the AC is the sum of AFC & AVC the graphical structure of the AC curve can be shown through the vertical addition of AFC curve & AVC curve.

At OM level of output, AFC = MA; AVC = MB

Hence AC at OM level = MA + MB = MC

Thus, point C on AC curve is derived.

At OV level of output, AFC = VH; AVC = VG

Hence AC at OV level = VH + VG =-VK

Thus, point K on AC curve is derived.

At ON level of output, AFC = NQ; AVC = NR

Hence AC at ON level = NQ + NR = NT

Thus, point on AC curve is derived. .

At OS level of output, AFC = SD; AVC = SE

Hence AC at OS level = SD + SE = SF

Thus, point F on AC curve is derived.

At length, by joining C, K, T, & F points, the shape of SAC curve can be derived & this shape is just like‘U’.

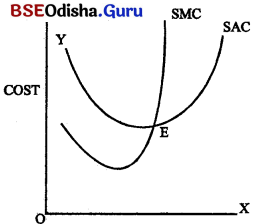

Question 3.

Discuss the relationship between Marginal cost & Average cost.

Answer:

In the short-run, the cost is classified into fixed cost & variable cost. As such, the total cost incurred for producing a given level of output is assessed as the combination of these total fixed cost & total variable cost. Considering the nature of total fixed cost (TFC), it is observed that there is no change in the TFC irrespective of the level of output & hence stands as a constant entity in the productive process during short-run. Regarding total variable cost (TVC), this cost changes with the change in the level of output & hence treated as “Prime cost” in the cost-structure during short- run.

Marginal Cost & its Nature.

Marginal cost which is enunciated by Austrian school of Economics refers to rate of change of total cost by producing one additional unit of output. The total cost, being the sum of TFC & TVC it increase with the increases in the level of output. Hence Marginal Cost (MC) is defined as an addition made to the total cost coused by an increase in one extra unit produced. Mathematically stated.

MCn = TCn – TCn-1

or, MC = \(\frac{\Delta \mathrm{TC}}{\Delta \mathrm{C}}\)

Where, n → no of units produced

Q → output

Marginal cost is viewed as an extra cost for producing one extra unit more or less. As during short-run, total fixed cost does not change under any circumstances, marginal cost being expressed as change in total cost is no way related to this total fixed cost. It is only associated with Total Variable Cost (TVC) which changes with the change in the level of output. Marginal cost at first stage decreases with the increase in the level of output & afterwards increases. So marginal cost curve is U-shaped.

Average Cost & its Nature :

In the short-run, Average Cost (AC) is also composed of AFC & AVC. It is the cost incurred per unit of output produced. Hence AC = \(\frac{TC}{Q}\)

Average cost breaks into AFC & AVC. AFC regularly decreases with increase in the level of output & AVC, at first stage decreases with the increase in the level of output & then increases with the increases in the level output. Like MC curve, AC curve is also U-shaped.

The nature & behaviour of the AC & MC can be explained with numerical example & graphical illustrations.

Numerical Analysis

| Units of Output (units) | Total Cost (in Rs.) | Average Cost (in Rs.) | Marginal Cost (in Rs.) |

| 1 | 40 | 40 | – |

| 2 | 60 | 30 | 20 |

| 3 | 70 | 23.3 | 10 |

| 4 | 76 | 19 | 6 |

| 5 | 84 | 16.8 | 8 |

| 6 | 96 | 16 | 12 |

| 7 | 112 | 16 | 16 |

| 8 | 136 | 17 | 24 |

| 9 | 162 | 18 | 26 |

The above numercial analysis indicates that the AC & MC both decreases with the increase in the level of output at the first phase of production But MC attains its minimum point much earlier than the AC (producing 4th unit). AC attains its minimum point while 7th unit is produced. At this level, MC = AC. Above this point MC < AC but afterwards AC < MC

The inference drawn with this analysis can also be explained with the help of graphical analysis. In the figure, OX-axis measures output & OY-axis measures cost. SAC & SMC represent short-run Average Cost & short-run Marginal Cost respectively. From the figure, it is obvious that upto the point E, AC > MC & AC is falling. At point E, (minimum point of AC curve) both AC & MC are equal after the point E, MC>AC & AC is increasing.

General Conslusion.

(a) Both Average cost & marginal cost can be calculated from Total cost i.e.

AC = \(\frac{TC}{Q}\) &MC = \(\frac{\Delta \mathrm{TC}}{\Delta \mathrm{Q}}\)

(b) When Average cost is falling, MC < AC (c) At the minimum point of AC, MC = AC (d) When AC is rising MC > AC

The above analysis has discussed the general inter-relationship between AC & MC.

Question 4.

Discuss the relationship among the Total Revenue, Average Revenue & Marginal Revenue.

Answer:

Revenue refers to the money income received from the sale of the product. It is the money receipts earned by the producer by selling its product in the market. Revenue can be expressed in three forms like Total Revenue, Average Revenue & Marginal Revenue.

(a) Total Revenue (TR) : Total Revenue refers to the sum total of income earned the sale of output. It is the total money receipts earned by the producer from the sale of its product. In other words, it is the sum of all sale, receipts or income of a firm.

Total Revenue can be calculated by multiplying price with the quantity sold.

TR = P × Q

P → Unit price

Q → Quantity sold

(b) Average Revenue (AR) : Average Revenue refers to the revenue earned per unit of output. It is the revenue earned by the seller/producer/firm by selling the per unit product. Average Revenue can be obtained by dividing the total revenue with number of units (Q) sold.

Thus, Average Revenue = AR = \(\frac{TR}{Q}\)

(c) Marginal Revenue (MR) : Marginal Revenue is the additional revenue earned from the sale of one extra unit of a good. In other words, it is the addition made to the TR by selling one extra unit of good. Thus, MR is the net revenue obtained from the sale of one additional unit. It is the change in the TR resulting from the sale of one more unit of good. Marginal Revenue can be obtained in the following way.

MRn = TRn – TRn-1

n → number of units sold

or, MR = \(\frac{\Delta \mathrm{TR}}{\Delta \mathrm{Q}}\)

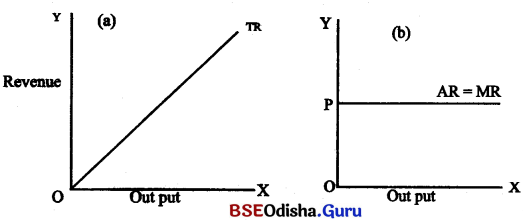

Relationship among TR, AR & MR : There exists certain basic relationship among TR, AR & MR. This relationship can be explained under two heads which are classified into perfect competitive market & imperfect market.

(a) Relationship under Perfect competition.

Perfect competition is said to exist when all the goods are homogenous & sold at a uniform price. The relation among there TR, AR & MR can be explained with the following numerical & graphical analysis.

NUMERICAL ANALYSIS

| Units of Output | AR (in Rs.) | TR (in Rs.) | MR (in Rs.) |

| 1 | 10 | 10 | 10 |

| 2 | 10 | 20 | 10 |

| 3 | 10 | 30 | 10 |

| 4 | 10 | 40 | 10 |

| 5 | 10 | 50 | 10 |

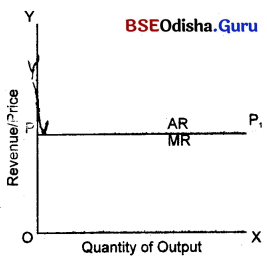

The above analysis reveals that under perfect competition AR or Price is uniform & hence MR becomes equal to AR. Total Revenue increases at a constant rate with the increase in the units of the product sold.

Graphical Analysis:

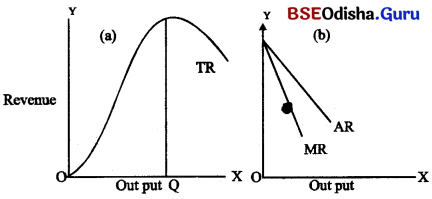

In the figure (a), it is observed that TR curve slopes upwards which established TR increase when more & more output are sold. The fig (b) indicates a horizontal straight line because of equality between AR & MR. AR curve coincides with MR due to this relationship.

(b) Relationship among TR, AR & MC under Imperfect Competition :

Under imperfect competition, AR gradually diminishes with the increase in the sale of output. It implies that if the sella” wants to sell more he is to reduce the price & vice – versa. Unlike the perfect competition price is not uniform. The relationship among TR, AR and MR is explained with the following example.

Numerical Analysis

| Units (in Rs.) | AR (in Rs.) | TR (in Rs.) | MR |

| 1 | 10 | 10 | 1o |

| 2 | 9 | 18 | 8 |

| 3 | 8 | 24 | 6 |

| 4 | 7 | 28 | 4 |

| 5 | 6 | 30 | 2 |

The analysis shows that AR gradually decreases with the increase in the sale of output, l R increases at a diminishing rate & MR gradually diminishes.

Graphical Analysis

The figure (a) indicates that TR increase at an increasing rate upto point & then increase at a diminishing rate. It implies that at the stage of diminishing returns TR increases at a diminishing rate & by selling OQ unit of output, it becomes maximum.

The figure (b) indicates that both AR & MR are falling with the increase in the number of units sold & AR is always greater than MR.

Thus, the relationship among TR & MR is found to be in different forms under different market structure.

![]()

Question 5.

Describe the nature of various revenue concepts under perfect competition & imperfect competition.

Answer:

Average Revenue (AR) refers to the revenue earned per unit of output. On the other hand marginal revenue refers to the addition made to the total revenue due to the additional sale of one unit, the nature of these differs from each other under different market conditions. In general, there exists certain relationship between these two concepts. But this relationship differs from market to market which is illustrates as follows :

(i) Perfect competition: Under perfect competition, individual firms are price-takers. They bring numerous exercise, no control and influence over the price. The price is determined by the industry as a whole which consists of a number of firms producing identical products. The price is determined by the interaction of market demand and supply for us. When all units of a product are sold at one price, the price equals to the average revenue and the average revenue equals to the marginal revenue. Therefore, under perfect competition the AR, MR and price become equal as shown in the following table.

| Price in Rs. | Quantity sold | TR in Rs. | AR in Rs. | MR |

| 5/- | 5 | 25 | 5 | – |

| 5/- | 6 | 30 | 5 | 5 |

| 5/- | 7 | 35 | 5 | 5 |

| 5/- | 8 | 40 | 5 | 5 |

| 5/- | 9 | 45 | 5 | 5 |

The table makes evident that when price is Rs.5/ per unit the total revenue is obtained by multiplying the price with the quantity sold. As more and more quantity is sold the total revenue increases but the AR and MR remain unchanged. The price paid by the consumer is the revenue of the seller. Since price equals to AR and MR the demand curve, AR curve and MR curve coincide as shown in the following diagram.

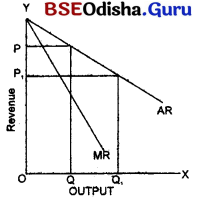

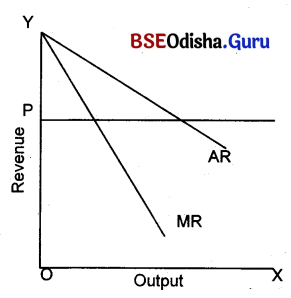

(ii) Monopoly : A pure monopoly market presents a situation which is exactly opposite of pure competition. A monopolist being the only one seller in respect of a particular commodity controls the supply of the product. There is no substitute to the monopolist’s product. He is the price-maker of his product as he has no rival. Therefore, by restricting his output he can change any price so as to take away the entire consumers expenditure on the commodity. He may boost up his sales by lowering the price of his product or he may raise the price by restricting the supply. Therefore, the average revenue slopes downwards from left to right. But his total revenue remains unchanged and the marginal revenue is zero. The marginal revenue coincides with the ‘X’ axis as shown in the following table and diagram.

| Price in Rs. | Unity sold in Rs. | TR in Rs. | AR in Rs. | MR in Rs. |

| 5 | 8 | 40 | 5 | 0 |

| 4 | 10 | 40 | 4 | 0 |

| 2 | 20 | 40 | 2 | 0 |

| 1 | 40 | 40 | 1 | 0 |

From the table it may be seen that the monopolist sells more units of his product by lowering the price but his total revenue remains unaffected. Hence, the marginal revenue curve coincides with OX axis as shown in the diagram:

In the diagram the AR curve represents unitary elasticity of demand suggesting that the total revenue of the firm is constant at OP and OP1 price, though sale increases from OQ to OQ1 as a result of fall in price from OP to OP1.

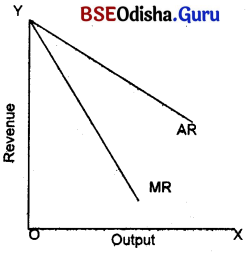

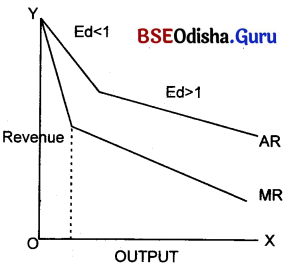

(iii) Imperfect competition: Under imperfect competition market consists of many categories ranging from two sellers to a large number of buyers and selling. In these markets the AR curve is less than perfectly elastic. The elasticity differs from market to market. The demand curve or AR curve has a downward slope. The downward slope of the AR curve indicates that the seller can sell more and more by lowering the price level and vice versa. The corresponding marginal revenue will be less than the falling average revenue. The MR curve will, therefore, lie below the AR curve as shown in the following table and diagram.

| Price | Quantity sold | TR | AR | MR |

| Rs. 5/- | 1 | 5 | 5 | 5 |

| Rs. 4/- | 2 | 8 | 4 | 3 |

| Rs. 3/- | 3 | 9 | 3 | 1 |

| Rs. 2/- | 4 | 8 | 2 | -1 |

| Rs. 1/- | 5 | 5 | 1 | -3 |

The table shows that as more and more quantity is sold at lower and lower prices the total revenue increases at a diminishing rate. The average revenue also goes on falling but the MR falls at a greater rate than the fall of AR.

The diagram shows that the AR curve falls as more quantity is sold at lower prices and MR curve lies below the AR curve as the former falls at a greater rate than the latter. In this connection it may be noted that when the seller restricts the supply to sell at higher prices the AR curve takes a positive slope which is represented by a rising AR curve. When the AR curve slopes upwards, as shown in the diagram, the MR curve also slopes upwards and lies above the AR.

In a market characterised as monopolistic competition there are many small sellers and buyers. The products are differentiated, although not exact substitutes. A seller under this market structure faces competition from rival sellers. He is a monopolist in the sense that some buyers have preference for his product. Taking advantage of this a seller can charge a little more than his rivals

and sellers or charge a little less and sell more. The AR curve facing a firm in this situation is quite elastic though not perfectly elastic as in pure competition. The AR, therefore, has a gentle slope. The MR curve which slopes downwards lies close to the AR an shown in the diagram:

The diagram shows that the AR curve under the.monopolistic competition being more than unitary elastic the MR curve lies to the right of the mid-point of the perpendicular drawn from the price axis to the AR curve

(iv) Oligopoly : In oligopoly market there is a small number of sellers. The price changed by one invites retaliation from others and the latter may not react to the change in price. If a seller rises the price and other do not follow then the former will face a fall in demand for his product and suffer loss. In such a case the AR curve appears less elastic in some portion and more elastic in another portion. The corresponding MR curve becomes discontinuous as shown in the diagram:

To sum up the AR under perfect competition takes horizontal shape and the MR curve coincides withAR curve. In pure monopoly the AR curve sloped down wards with unitary elasticity throughout its length and the MR curve coincides with the OX horizontal axis.

The AR curve under imperfect competition has a negative slope and the MR curve lies below the AR curve.

Under monopolistic competition AR slopes downwards with more than unitary elasticity and the MR slopes downwards and lies close to the AR.

Under oligopoly the AR curve is indeterminate. It usually takes kinked shape and the MR, which lies below AR becomes discontinuous and slopes downwards at the point of kink.

Group – C

Objective type Questions with Answers

I. Multiple Choice Questions with Answers :

Question 1.

The price paid for the use of factor input is called

(i) factor price

(ii) value of factor

(iii) cost of production

(iv) price of input

Answer:

(iii) cost of production

Question 2.

The functional relationship between cost of production & output is called

(i) production function

(ii) consumption function

(iii) cost function

(iv) All of the above

Answer:

(iii) cost function

Question 3.

Cost is always expressed for a

(i) particular price of a factor

(ii) particular time period

(iii) particular quantity of a factor

(iv) None of the above

Answer:

(ii) particular time period

Question 4.

Change in cost of production occurs due to

(i) change in the level of output

(ii) Change in factor proportion

(iii) change in factory size

(iv)

Answer:

(i) change in the level of output

Question 5.

Cost in economics indicates

(i) only money case

(ii) only real cost

(iii) only economic cost

(iv) only real cost

Answer:

(iii) only economic cost

Question 6.

Money cost is otherwise known as

(i) normal cast

(ii) Prime cost

(iii) overhead cost

(iv) Supplementary cost

Answer:

(i) normal cast

Question 7.

Efforts, pain, sacrifices, troubles etc undertaken by the society due to production is termed as

(i) supplementary cost

(ii) opportunity cost

(iii) real cost

(iv) prime cost

Answer:

(iii) real cost

Question 8.

Producers do not generally bear

(i) Real cost

(ii) supplementary cost

(iii) Alternative cost

(iv) None of the above

Answer:

(i) Real cost

Question 9.

Economic cost comprises of both

(i) Money cost & Real cost

(ii) Explict cost & implicit cost

(iii) Prime cost & overhead cost

(iv) All of the above

Answer:

(ii) Explict cost & implicit cost

Question 10.

Money cost is basically

(i) Accounting cost

(ii) Explicit cost

(iii) implicit cost

(iv) Both (i) and (ii)

Answer:

(iv) Both (i) and (ii)

Question 11.

Real cost is generally borne by the

(i) Enterprereurs

(ii) workers

(iii) Members of the society

(iv) Government

Answer:

(iii) Members of the society

Question 12.

Rent for the self owned building for business is covered under

(i) money cost

(ii) real cost

(iii) opportunity cost

(iv) Both (i) and (ii)

Answer:

(iv) Both (i) and (ii)

Question 13.

The amount from the next best alternative use of a factor which is foregone is called

(i) alternative cost

(ii) supplementary cost

(iii) opportunity cost

(iv) Both (i) and (ii)

Answer:

(i) alternative cost

Question 14.

Suppose a piece of land be best be used for cultivating rice, potato, wheat & sugarcane. Frame rice, it earns 10,000, from potato it earns 15,000 from wheat it earns 9,000. & from sugar cane it earn, 12,000. If it is now used for producing potato, what will be its opportunity cost ?

(i) 15,000

(ii) 10,000

(iii) 12,000

(iv) 9,000

Answer:

(iii) 12,000

Question 15.

Salary of the manager is

(i) variable cost

(ii) fixed cost

(iii) real cost

(iv) None of the above

Answer:

(ii) fixed cost

Question 16.

If the level of output of a factory becomes zero its fixed cost becomes

(i) zero

(ii) decreases

(iii) increases

(iv) remains unaffected

Answer:

(iv) remains unaffected

Question 17.

If the level of output of a unit continuously goes on diminishing, its fixed cost shall

(i) diminish

(ii) remain unchanged

(iii) first diminish & then increase

(iv) become zero

Answer:

(ii) remain unchanged

Question 18.

Which cost remains unaffected irrespective of the level of output

(i) Supplementary cost

(ii) fixed cost

(iii) variable cost

(iv) Both (i) and (ii)

Answer:

(i) Supplementary cost

Question 19.

If the level of output of a factory goes on increasing, the fixed cost curve of it will

(i) slope upward from left toright

(ii) slope downward from left to right

(iii) become a vertical straight line

(iv) become a horizontal straight line

Answer:

(iv) become a horizontal straight line

Question 20.

The elasticity of the fixed cost curve is

(i) perfectly elastic

(ii) perfectly inelastic

(iii) unitary elastic

(iv) relatively more inelastic

Answer:

(i) perfectly elastic

Question 21.

Fixed cost is otherwise known as

(i) prime cost

(ii) supplementary cost

(iii) alternative cost

(iv) none of the above

Answer:

(iii) alternative cost

Question 22.

The emergence of fixed cost & variable cost occurs during

(i) long period

(ii) short-period

(iii) market period

(iv) All of the above

Answer:

(ii) short-period

Question 23.

Variable cost its otherwise known as

(i) prime cost

(ii) alternative cost

(iii) supplementary cost

(iv) overhead cost

Answer:

(i) prime cost

Question 24.

At the initial stage of production if the level of production increases, the average variable cost

(i) increases

(ii) decreases

(iii) remains unaffected

(iv) none of the above

Answer:

(ii) decreases

Question 25.

The shape of the average variable cost is generally

(i) ‘L’ shaped

(ii) ‘V’ shaped

(iii) ‘U’ shaped

(iv) none of the above

Answer:

(iii) ‘U’ shaped

Question 26.

If the level of output increases, the average fixed cost

(i) remains fixed

(ii) decreases

(iii) increases

(iv) both (i) and (ii)

Answer:

(iii) increases

Question 27.

AFC curve takes the shape of a

(i) ‘U’

(ii) L

(iii) Rectangular hyperbola

(iv) Straight line

Answer:

(iii) Rectangular hyperbola

Question 28.

At different levels of output, the total fixed cost

(i) remains constant

(ii) goes on increasing

(iii) goes on diminishing

(iv) first increases & then decreases

Answer:

(i) remains constant

Question 29.

When AC is falling marginal coat curve remains

(i) above the AC curve

(ii) below the AC curve

(iii) constant

(iv) none of the above

Answer:

(ii) below the AC curve

Question 30.

Firm has to bear the loss of

(i) variable cost

(ii) fixed cost

(iii) real cost

(iv) money cost

Answer:

(i) variable cost

Question 31.

Interest on capital borrowed is an example of

(i) alternative cost

(ii) fixed cost

(iii) real cost

(iv) variable cost

Answer:

(ii) fixed cost

Question 32.

Payment forth raw material is an example of

(i) fixed cost

(ii) variable coal

(iii) alternative cost

(iv) real cost

Answer:

(ii) variable cost

Question 33.

Insurance premium of a company is an example of

(j) fixed cost

(ii) variable cost

(iii) real cost

(iv) none of the above

Answer:

(i) fixed cost

Question 34.

Cost per unit of output is called

(i) total cost

(ii) average cost

(iii) marginal coat

(iv) none of the above

Answer:

(ii) average coat

Question 35.

Addition made to the total cost is called

(i) average cost

(ii) supplementary cost

(iii) marginal cost

(iv) All of the above

Answer:

(iii) marginal cost

Question 36.

AC becomes equal to MC when

(i) AC curve cuts MC from below

(ii) AC curve cuts MC at its minimum point.

(w) MC curve cuts AC at its minimum point

(iv) AC curve cuts MC curve from above

Answer:

(iii) MC curve cuts AC at its minimum point

Question 37.

Under perfect competition. AR becomes

(i) greater than MR

(ii) leas than AR

(iii) equal toAR

(iv) can not say

Answer:

(iii) equal to AR

Question 38.

Under pefect competition AR curve takes the shape of a

(i) rectanugal hyperbola

(ii) horizontal straight line

(iii) vertical straight line

(iv) U – shaped

Answer:

(ii) horizontal straight line

Question 39.

Under monopoly, AR curve lies

(i) above the MR curve

(ii) below the MR curve

(iii) equal to MR curve

(iv) none of the above

Answer:

(i) above the MR curve

Question 40.

MC is not related with

(i) fixed cost

(ii) variable cost

(iii) alternative cost

(iv) real cost

Answer:

(ii) variable cost

Question 41.

If AR = MR, AR curve and MR curve become :

(i) Parallel to OY axis

(ii) Parallel to OX axis

(iii) All of the above

(iv) None of the above

Answer:

(ii) Parallel to OX axis

![]()

Question 42.

Under perfect competition AR is :

(i) AR = MR

(ii) AR is less than MR

(iii) AR is greater than MR

(iv)

Answer:

(i) AR = MR

Question 43.

Average revenue generally indicates :

(i) MR

(ii) TR

(iii) Price

(iv) Both(i) and (ii)

Answer:

(iii) Price

Question 44.

Average Revenue is equal to :

(i) TR-Te

(ii) TRn – TRn-1

(iii) TR/Q

(iv) None of the above

Answer:

(iii) TR/Q

Question 45.

TR is maximum when :

(i) MR is maximum

(ii) MR is zero

(iii) All of the above

(iv) None of the above

Answer:

(ii) MR is zero

Question 46.

Total Revenue at any output is equal to :

(i) Cost per unit multiplied by quantity sold.

(ii) Price per unit multiplied by quantity sold.

(iii) Both (i) and (ii)

(iv) None of the above.

Answer:

(ii) Price per unit multiplied by quantity sold.

Question 47.

If MR is negative, TR remains :

(i) Constant

(ii) Rises

(iii) Falls

(iv) None of the above.

Answer:

(iii) Falls

Question 48.

MRn is :

(i) MRn – TRn – TRn-1

(ii) MRn = TRn-1 – TRn

(iii) MRn – ARn – ARn-1

(iv) None of the above.

Answer:

(i) MRn – TRn – TRn-1

Question 49.

Under Monopoly, MR is always.

(i) Greater than AR

(ii) Less than AR

(iii) Both (i) and (ii)

(iv) None of the above

Answer:

(ii) Less than AR

Question 50.

The incremental cost is associated with

(i) total cost

(ii) average cost

(iii) marginal cost

(iv) all of the above

Answer:

(iii) marginal cost

II. Fill in the blanks :

Question 1.

____ function describes the functional relationship between output and cost.

Answer:

Cost

Question 2.

____ costs are nominal costs.

Answer:

Money

Question 3.

Insurance charges are the example of ____ costs.

Answer:

money

Question 4.

Advertising Cost is the example of ____ cost.

Answer:

explicit

Question 5.

Payments for raw materials are ____ costs.

Answer:

explicit

Question 6.

____ Cost includes only explicit cost.

Answer:

Accounting

Question 7.

____ Cost is deducted from total revenue to calculate Gross Profit.

Answer:

Accounting

Question 8.

Net Profit is the difference between total revenue and ____ costs.

Answer:

Economic

Question 9.

Real cost is ____ cost.

Answer:

implicit

Question 10.

Total Variable Cost is ____ when the output is zero.

Answer:

zero

Question 11.

The wage paid to security personnel is ____ cost.

Answer:

Fixed Cost.

Question 12.

Total Variable Cost is inverted ____

Answer:

‘S’ shaped.

Question 13.

____ are‘Overhead Costs’.

Answer:

Fixed Costs

Question 14.

____ cost is prime cost.

Answer:

Variable

Question 15.

Fixed Costs are realised during ____ period

Answer:

Short

Question 16.

AFC ____ throughout with the increase in output.

Answer:

falls

Question 17.

AVC first ____ and then rises.

Answer:

diminishes

Question 18.

AC is ____ shape.

Answer:

U-shaped

Question 19.

Rate of change of Variable Cost for producing one more unit of output is called ____

Answer:

MC

Question 20.

MC cuts AC curve at its ____ point.

Answer:

minimum

Question 21.

____ Revenue at any point is equal to price per unit multiplied by quantity sold.

Answer:

Total

Question 22.

____ Revenue is the revenue per unit of output.

Answer:

Average

Question 23.

Marginal Revenue is the change in ____ Revenue resulting from the sale of one more unit of output.

Answer:

Total

Question 24.

If MR is negative, TR ____

Answer:

falls.

Question 25.

TR is maximum when MR is ____

Answer:

zero.

Question 26.

Under Imperfect Competition, TR ____ at an diminishing rate.

Answer:

increases

Question 27.

Under Perfect Compeition AR = ____

Answer:

MR.

![]()

Question 28.

Under monopoly, AR is always ____ than MR.

Answer:

greater

Question 29.

____ revenue generally indicates price.

Answer:

Average

Question 30.

____ = \(\frac{TR}{Q}\)

Answer:

AR

III. Correct the Sentences :

Question 1.

The quantity of output produced increases with the increase in cost of production.

Answer:

Incorrect:

Correct: Cost of production increases with the increase in quantity of output produced

Question 2.

Cost of production relates to demand for goods.

Answer:

Incorrect:

Correct: Cost of production relates to supply of goods.

Question 3.

Real cost is known as nominal cost.

Answer:

Incorrect

Correct: Money cost is known as nominal cost.

Question 4.

Accounting costs include both explicit & implicit cost.

Answer:

Incorrect.

Correct: Accounting costs include only explicit cost.

Question 5.

Transportation cost is a money cost.

Answer:

Correct:

Question 6.

Economic cost covers only explicit cost.

Answer:

Incorrect:

Correct: Economic cost covers both explicit & implicit cost.

Question 7.

Accounting cost is a broad concept but economic cost is a narrow concept.

Answer:

Incorrect:

Correct: Economic cost is a broad concept but accounting cost is a narrow concent.

Question 8.

Money cost is a subjective concept.

Answer:

Incorrect:

Correct: Real cost is a subjective concept.

Question 9.

Money cost is same as real cost.

Answer:

Incorrect:

Correct: Money cost is different from Real cost.

Question 10.

Money cost is a qualitative concept whereas real cost is a quantitative concept.

Answer:

Incorrect:

Correct: Real cost is a qualitative concept whereas money cost is a quantitative concept.

Question 11.

Money cost is otherwise called social cost.

Answer:

Incorrect:

Correct: Real cost is otherwise called social cost.

Question 12.

Real cost is not borne by the producer.

Answer:

Correct.

Question 13.

Money cost is expressed in terms of efforts & sacrifices.

Answer:

Incorrect:

Correct: Real cost is expressed in terms of efforts & sacrifices.

Question 14.

Opportunity cost is transfer cost.

Answer:

Correct.

Question 15.

Real cost is explicit cost.

Answer:

Incorrect :

Correct: Real cost is implicit cost.

Question 16.

Gross profit is calculated by deducting accounting cost from Total Revenue.

Answer:

Correct

Question 17.

Net Profit is calculated by deducting explicit cost from total revenue.

Answer:

Incorrect:

Correct: Net Profit is calculated by deducting economic cost from total revenue.

Question 18.

Fixed cost increases with the increase in the level of output.

Answer:

Incorrect:

Correct: Variable cost increases (or fixed cost remains samel with the increase in the level of output.

Question 19.

Fixed cost is independent of level of output.

Answer:

Correct:

Question 20.

Variable costs are supplementary cost.

Answer:

Incorrect:

Correct: Fixed cost are supplementary cost.

Question 21.

Fixed costs are direct costs.

Answer:

Incorrect:

Correct: Variable costs are direct costs.

Question 22.

Fixed costs are otherwise known as overhead costs.

Answer:

Correct:

Question 23.

Fixed costs become zero when the level of output is zero.

Answer:

Incorrect:

Correct: Fixed cost is positive when the level of output is zero.

Question 24.

Fixed costs are prime costs.

Answer:

Incorrect:

Correct: Variable costs are prime costs.

Question 25.

Insurance charges are real costs.

Answer:

Incorrect:

Correct: Insurance charges are money costs.

![]()

Question 26.

Salary of executives is a variable cost.

Answer:

Incorrect:

Correct: Salary of excutives is a fixed cost.

Question 27.

The shape of AC curve is U-shaped.

Answer:

Correct:

Question 28.

Average cost is equal to marginal cost at the maximum point of average cost.

Answer:

Incorrect:

Correct: Average cost is equal to marginal cost at the minimum point of average cost.

Question 29.

Average cost first increases & then decreases with the increase in the level of output.

Answer:

Incorrect:

Correct: Average cost first decreases & the increases with the increase in the level of output.

Question 30.

Marginal cost is associated with fixed cost in the short-run

Answer:

Incorrect:

Correct: Marginal cost is associated with variable cost in the short-run.

Question 31.

Average cost cuts marginal cost curve at its minimum point.

Answer:

Incorrect:

Correct: Marginal cost cuts average cost at its minimum point.

Question 32.

When AC is equal to MC, AC is minimum

Answer:

Incorrect:

Correct: When AC is equal to MC, AC is maximum.

Question 33.

When AC is less than MC, the AC must be falling.

Answer:

Correct

Question 34.

When AC is more than MC. AC must be falling.

Answer:

Correct

Question 35.

Average fixed cost is independent of level of output.

Answer:

Incorrect:

Correct: Total fixed cost is independent of level of output.

Question 36.

AFC is fixed with the increase in level of output.

Answer:

Incorrect

Correct: AFC decreases with the increase in the level of output.

Question 37.

Average cost changes faster than marginal cost.

Answer:

Incorrect

Correct: Marginal cost changes faster than average cost.

Question 38.

Fixed cost arises only in the long-run.

Answer:

Incorrect

Correct: Fixed cost arises only in the short-run.

Question 39.

All the costs are variable in the long run

Answer:

Correct

Question 40.

Total revenue represents price of the goods.

Answer:

Incorrect

Correct: Average revenue represents price of goods.

Question 41.

Average revenue curve is the demand curve.

Answer:

Correct:

Question 42.

In perfect competition, AR>MR.

Answer:

Incorrect:

Correct: In perfect competition AR = MR.

Question 43.

AR increases with the increase in the units of output sold in a perfectly competitive market.

Answer:

Incorrect:

Correct: AR regains same with the increase in the units of output sold in a perefectly competitive market.

Question 44.

Under monopoly, AR < MR.

Answer:

Incorrect:

Correct: Under monopoly, AR > MR

Question 45.

In imperfect market AR increases with the increase in the sale of output.

Answer:

Incorrect:

Correct: In Imperfect market AR decreases with the increase in the sale of output.

Question 46.

Total Revenue at any output is equal to cost per unit multiplied by quantity sold.

Answer:

Incorrect.

Correct: Total Revenue at any point is equal to price per unit multiplied by quantity sold.

Question 47.

Average Revenue is the revenue per unit of output.

Answer:

Correct.

Question 48.

Marginal Revenue is the change in average revenue resulting from the sale of one more unit of output.

Answer:

Incorrect.

Correct : Marginal Revenue is the change in Total Revenue resulting from the sale of one more unit of output.

Question 49.

If MR is negative, TR remains constant.

Answer:

Incorrect.

Correct: If MR is negative, TR falls.

Question 50.

TR is maximum when MR is maximum.

Answer:

Incorrect.

Correct: TR is maximum when MR is zero.

Question 51.

Under Imperfect Competition, TR increases at an increasing rate.

Answer:

Incorrect.

Correct: Under Imperfect Competition, TR increases at an diminishing rate.

![]()

Question 52.

If AR = MR, AR curve and MR curve become parallel to OX-axis.

Answer:

Correct.

Question 53.

Under Perfect Competition, AR is greater than MR.

Answer:

Incorrect.

Correct: Under Perfect CompeitionAR = MR.

Question 54.

Under Monopoly, MR is always greater than AR.

Answer:

Incorrect.

Correct: Under monopoly, AR is always greater than MR.

Question 55.

Marginal Revenue generally indicates price.

Answer:

Incorrect.

Correct: Average revenue generally indicates price.

Question 56.

AR = TR-TC

Answer:

Incorrect.

Correct: AR = \(\frac{TR}{Q}\)

IV. Answer the following questions in one word :

Question 1.

What does cost function show ?

Answer:

Cost function shows the functional relationship between cost of production & quantity of output produced.

Question 2.

What is cost of production ?

Answer:

Cost of production refers to the expenses incurred for producing a given level of output.

Question 3.

Which cost is called “Nominal Cost” ?

Answer:

Money cost is called “Nominal cost”.

Question 4.

What is money cost ?

Answer:

The cost of production expressessed in terms of money is called money cost.

Question 5.

What do you mean by accounting cost ?

Answer:

Accounting cost is explicit cost whose accounts can be maintained.

Question 6.

What is a difference between explicit cost & implicit cost ?

Answer:

Explicit cost can be expressed in any form but implicit cost is a hidden cost not expressible.

Question 7.

What is economic cost ?

Answer:

Economic cost is the sum of explicit cost & implicit cost.

Question 8.

Give an example of implicit cost.

Answer:

Payment for entrepreneur’s self invested capital.

Question 9.

How is the net profit calculated ?

Answer:

Net profit is calculated by deducting economic cost from total revenue.

Question 10.

What is real cost ?

Answer:

Real costs are the efforts & sacrifices, troubles, pain etc. undergone for producing a commodity.

Question 11.

Which cost is called social cost ?

Answer:

Real cost is called social cost.

Question 12.

For which cost no real payment is made ?

Answer:

For real cost no real payment is made.

Question 13.

Which cost is direct cost ?

Answer:

Money cost is direct cost.

Question 14.

What is opportunity cost ?

Answer:

Opportunity cost is the cost for the next best alternative good which is foregone.

Question 15.

Which cost is called transfer cost ?

Answer:

Opportunity cost is called transfer cost.

Question 16.

What is fixed cost ?

Answer:

Fixed cost is that cost incurred for hiring fixed factors.

Question 17.

What happens to fixed cost when the level of output increases ?

Answer:

Fixed cost remains unchanged when the level of output increases.

Question 18.

What happens to fixed cost if the level of output is zero ?

Answer:

Fixed cost remains unchanged even at zero level of output.

Question 19.

What is variable cost ?

Answer:

Variable cost refers to that cost incurred for hiring variable factor.

Question 20.

Which cost is called supplementary cost ?

Answer:

Fixed cost is called supplementary cost.

![]()

Question 21.

Which cost is called overhead cost ?

Answer:

Fixed cost is called overhead cost.

Question 22.

What is other name of variable cost ?

Answer:

Prime cost is the other name of variable cost.

Question 23.

What happens to variable cost at zero level of output ?

Answer:

Variable cost becomes zero at zero level of output.

Question 24.

What is marginal cost ?

Answer:

Marginal cost is the additional cost incurred for producing one extra unit of good.

Question 25.

What happens to marginal cost if average cost is falling ?

Answer:

Marginal cost is less than average cost if average cost is falling.

Question 26.

What happens to average cost if MC > AC ?

Answer:

Average cost must be rising if MC > AC.

Question 27.

At what point of AC curve, MC curve intersects ?

Answer:

MC curve cuts at the minimum point of the AC curve.

Question 28.

What is revenue ?

Answer:

Revenue refers to the income earned by the producer from the sale of output.

Question 29.

Which concept of revenue represents price ?

Answer:

Average revenue represents price.

Question 30.

Which revenue curve is treated as demand curve ?

Answer:

AR curve is treated as demand curve.

Question 31.

What is the nature of AR under perfect competition ?

Answer:

AR remains same under perfect competition.

Question 32.

What is the reltion between AR & MR under perfect competition ?

Answer:

AR = MR under perfect competition.

Question 33.

What is shape of AR curve under perfect competition ?

Answer:

AR curve is a horizontal straight line under perfect competition.

Question 34.

What is the shape of AR curve in imperfect market ?

Answer:

In imperfect market, AR curve slopes downward from left to right.

Question 35.

What is the relation between AR & MR under imperfect competition ?

Answer:

Under imperfect competition, AR > MR.

Question 36.

What do you mean by ‘revenue’ ?

Answer:

Revenue refers to the income earned by the firm from the sale of its output.

Question 37.

What is TR?

Answer:

TR referse to sum of all types of income earned by the firm from the sale of output.

Question 38.

What is Marginal Revenue (MR) ?

Answer:

Marginal Revenue is the change in total revenue resulting from the sale of one more unit of output.

Question 39.

Under what circumstances AR curve and MR curve become a horizontal straight line and coincide with each other ?

Answer:

AR and MR curves coincide with each other and become a horizontal straight line under perfect competition.

Question 40.

What is the relationship between AR and MR under imperfect competition (monopoly) ?

Answer:

Under imperfect competition (monopoly) AR is greater than MR.

![]()

Question 41.

What is the significance of the revenue curves ?

Answer:

The significance of the revenue curve is observed in case of estimation of profits and losses, equilibrium of firm and price-changes.

Question 42.

Which concept of revenue is called Price ?

Answer:

Average Revenue is the same thing as price.

Question 43.

When AR is constant, what is the state of MR ?

Answer:

When AR is constant, MR is also constant and equal to AR.

Question 44.

What is the shape of MR and AR curve under Perfect Competition ?

Answer:

Under Perfect Competition both MR and AR curves are represented by one curve which is parallel to OX-axis.

Question 45.

How are the MR and AR curves under monopoly ?

Answer:

Under monopoly, MR and AR curves are separate from each other and both are downward sloping.